2020 has been a challenging year for so many different reasons. A pandemic that is sweeping the globe, and doing enormous economic damage to the United States. Tens of millions of Americans out of work, with no end in sight for many in especially hard hit industries like airlines, hotels, restaurants, tourism, and brick and mortar retail. I’m sure by this time, each and every one of us knows someone who has seen their livelihood destroyed or their health impaired by Covid-19. For many of these factors, it has proven difficult to blog about personal finance from a position of privilege. I have two secure jobs that I can do effectively from home, in fact, I think I’m even more productive working from home than I ever was while in the office.

For many years, I was a low-wage worker in the restaurant and retail industries and know that if I were still employed in those jobs I’d likely be laid off or have a substantially increased risk of contracting Covid-19 while working for near minimum wage. I’d be facing eviction, hunger, and the stress of not knowing where my next paycheck would be coming from. I won the career lottery, but so many of my friends and former colleagues did not and it pains me to know they are struggling.

As the clock ticks down on 2020, it appears that the enhanced stimulus payment of $2,000 in the United States will not pass in the Senate and provide the much needed financial assistance to struggling households. Republican politicians like John Cornyn brag on social media about eating a $125 steak, while denying extra stimulus to their constituents that are waiting in hours-long food pantry lines. It’s frustrating and quite unconscionable that in the supposedly richest nation on earth, a large portion of our politicians won’t even fully support our people like many other countries have done for theirs.

The Recovery

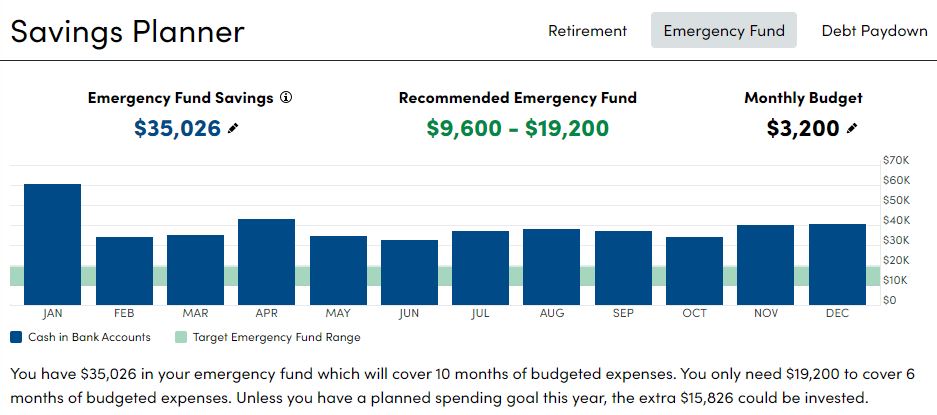

I am hopeful that 2021 will bring most of the lost jobs back and see an economic recovery that will benefit the working class. In a very odd twist, the stock market has rewarded the wealthy with strong gains in the last six months of the year, but the working class has yet to recover at all. This unfortunate trend has been exploding the wealth gap in the United States for a while now and there appears to be no end in sight. If there is anything this pandemic has proved, it is that the government will not save you (unless you are a powerfully connected corporation) and it is imperative to have a substantial emergency fund to protect yourself in the event of another economic catastrophe. Suze Orman has even started recommending people keep a 12-month emergency fund after seeing how the government has handled the situation and left so many families struggling 9 months into the pandemic. I use Personal Capital to keep an eye on my emergency fund and retirement savings goals and I am always being told that I am keeping too much in cash and missing out on higher investment returns because of it.

As you can see above, my recommended emergency fund, according to Personal Capital, is three to six months of expenses and I have 10 months of expenses saved. Assuming the extra $16,000 that Personal Capital thinks I should be investing earns 7%, that’s an extra $1,120 per year. This is where it becomes difficult to continue keeping “too much” in an emergency fund. But, when the alternative is exhausting the funds and resorting to credit cards at 25-30% APR to make ends meet after a long-term economic disaster, it seems like a small tradeoff to make for some extra peace of mind. Perhaps in 2021, this is an area that I can explore to find some reasonably safe and liquid options to squeeze a bit more of a return out of my emergency fund to keep up with inflation.

What’s Next?

While I am not usually one for making new year’s resolutions, I think it is important to do so heading into 2021 after the rough year we all had in 2020. With a much more sedentary and isolated life I’ve been living since March, it means I’ve let some things slip. While it would seem that all the extra “free time” from not having to commute would pay off in being able to tackle other goals, it turns out that I am actually spending more time working now that I am doing all my work from home. It’s not just me, as the Wall Street Journal also found that employees working from home are simply spending more time working now than before the pandemic. After spending 10 hours in front of the computer working all day, it is far to easy to simply walk 10 feet to the couch and watch Neflix and eat dinner, then head to bed. This is a habit that I need to break and my expanding waistline will thank me for it. I know I’m not the only one who gained the “Covid 20” this year after leading a life of sedentary isolation.

Personally, I aim to blog more, learn piano, and lose more (weight) in the next year. Let’s leap into 2021 with a plan to make it the best year we can!