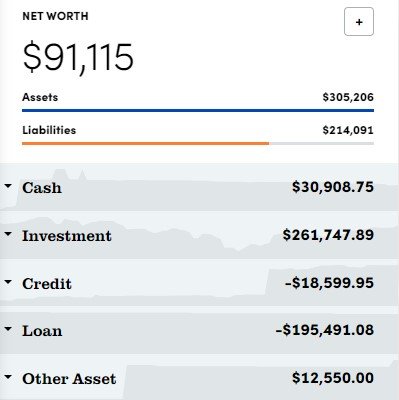

Let’s have a look at where my net worth settled on November 1st:

Net Worth = Assets minus Liabilities

| Assets | Amount | Change from Last Month |

| Checking/Savings | $30,909 | |

| Retirement Accounts | 197,301 | |

| Taxable/Nontax Investments | 64,447 | |

| Misc. (Gold/Silver/Cash/Collectibles) | 12,550 | |

| Total Assets | 305,206 | +19,073 |

| Liabilities | Amount | Change from Last Month |

| Credit Cards | $18,600 | 0% interest rate. |

| Student Loans | 195,491 | |

| Total Liabilities | 214,091 | +2,501 |

Net Worth = $91,115

Change in Net Worth from last month: +$16,573

Total Change in Net Worth Since July 2020: +$139,343

Net Worth Summary

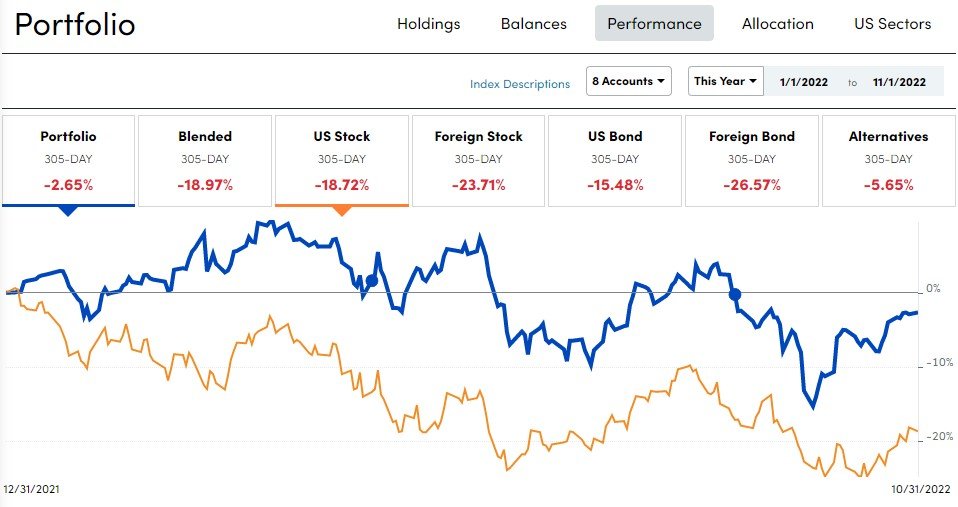

This past month has completely reversed the drop in net worth I posted in my last net worth update. As my net worth is now completely dependent on stock market direction, it has become much more volatile without the regular $3000-4000 per month I was adding to my investment balances before quitting my job. During my current “sabbatical” from the workforce, I’m keeping my spending low and investing in sectors that I believe will outperform over the next several years.

One thing that is beginning to look more appealing is moving my cash balance to an account with a 3% interest rate. With the Federal Reserve aggressively raising interest rates, many online banks are now paying significantly higher rates on savings account balances than the large brick and mortar banks. I am currently holding about $40,000 in checking, savings, and cash balances that are not really earning much and another $15,000 in cash equivalents or easily converted balances in other accounts. Since I am utilizing a 0% APR promotion on a couple of credit cards for 15 months, I can move the cash I would be using to pay those balances into a High Yield savings account to make a profit from borrowing free money from American Express and Citibank. At a 3% APR that would be about a $600 profit over the next 12 months with this strategy.

I am awaiting another large re-rating in the overall equity market in the coming months as the Federal Reserve’s hawkish intentions are fully realized by investors. The Federal Reserve’s primary mandate is inflation targeting and I don’t believe they will slow down the rate hikes until they’ve beaten inflation into submission – and that means demand destruction will have a negative impact on company’s future earnings expectations.

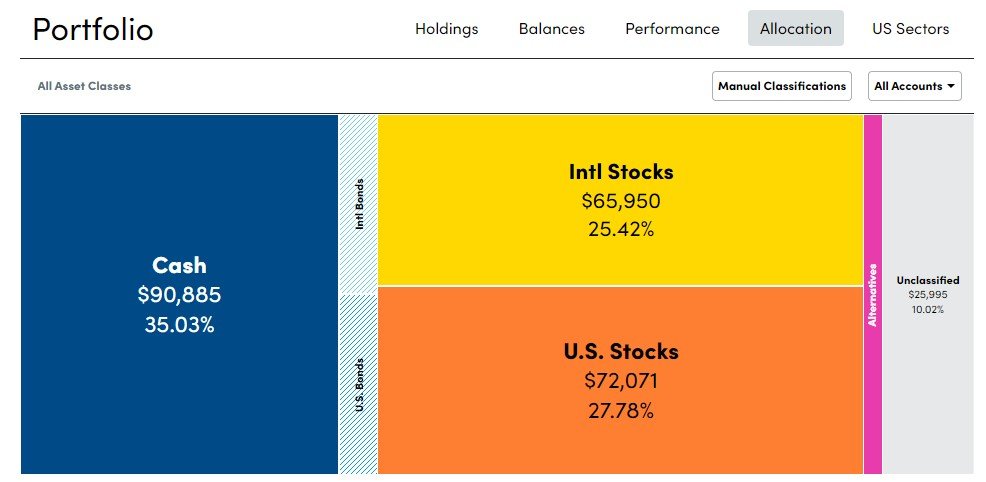

I have a disproportionately large holding of cash while awaiting what I expect to be a tremendous buying opportunity within the next three to six months in U.S. equities. The remaining allocations of 25% international stocks is entirely comprised of Canadian Oil and Gas companies that have been performing tremendously well this year as they de-lever their balance sheets and return significant cash to shareholders via stock buybacks and dividends.

The 28% in U.S. stocks is mostly made up of shares of Activision Blizzard, which is a merger arbitrage investment as it currently trades at a 30% discount to the cash purchase price being paid to them by Microsoft by the middle of 2023. Warren Buffett’s Berkshire Hathaway has also been following this merger arbitrage strategy to the tune of 9.5% of the outstanding shares. The remaining holdings in that U.S. stocks allocation are what has been dragging returns down, along with everyone else this year.