This is a month I’ve been looking forward to since starting to document my financial progress on The Money Sloth. I finally have a positive net worth! It’s almost surreal to suddenly go from over a decade of having a negative net worth due to a massive amount of student loan debt, to actually having more assets than liabilities. Hindsight is 20/20 and there are many things I would have done differently with regards to borrowing for college and grad school, but that’s water under the bridge now. Part of my motivation for embracing FIRE is the natural appeal it had to me as a longtime semi-extreme couponer. I never went to the extremes like the people featured on TV, but I took pride in keeping my grocery bills low.

Finally Reaching a Positive Net Worth!

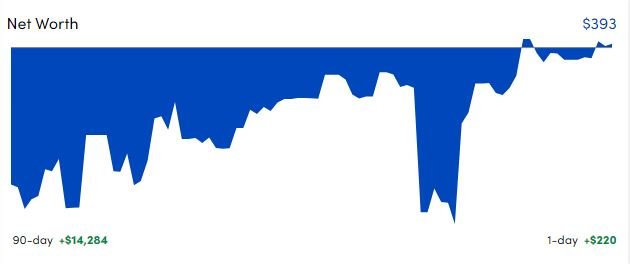

After really cranking up my savings rate starting in 2019, I now have a net worth of $393 in May 2021! This is an increase of $3,995 from last month and $48,621 since I started The Money Sloth Blog in July 2020.

Net Worth = Assets minus Liabilities

| Assets |

Amount |

Change from Last Month |

| Checking/Savings |

$42,757 |

|

| Retirement Accounts |

145,988 |

|

| Taxable Investments |

3,326 |

|

| Misc. (Gold/Silver/Cash/Collectibles) |

7,500 |

|

| Total Assets |

199,571 |

+826 |

| Liabilities |

Amount |

Change from Last Month |

| Credit Cards |

$2,012 |

|

| Student Loans |

197,165 |

|

| Total Liabilities |

199,177 |

-3,170 |

Net Worth = +$393

Change in Net Worth from last month: +$3,995

Total Change in Net Worth Since July 2020: +$48,621

The strange dip in the graph above is a period during which my private student loans were being refinanced and the linked accounts both showed a positive debt balance for a short while.

The strange dip in the graph above is a period during which my private student loans were being refinanced and the linked accounts both showed a positive debt balance for a short while.

Missing the Cryptocurrency Surge

I am not invested in any cryptocurrency, so I’ve apparently missed the bandwagon on Dogecoin. Honestly, I remember looking at Bitcoin back when it was $200/coin and there just wasn’t an easy way to acquire it back then without setting up their default wallet and transacting on some rather sketchy marketplaces. Obviously that has all changed and there are numerous places to buy and sell cryptocurrencies and that has likely contributed to these soaring valuations, with Bitcoin recently exceeding $60,000 each.

Will I live to regret not putting a portion of my net worth into crypto? Not likely as I don’t see it as a viable long-term investment. Dogecoin, for example, has an unlimited supply of coins that can be minted which will put downward pressure on prices over time. Bitcoin, on the other hand, has a hard cap on the number of coins in circulation, but the cost to transact on the Bitcoin blockchain is slow and expensive to facilitate regular commerce. I do believe the recent stalling of gold prices is tied to Bitcoin being used as an alternative store of value though. This trend may continue for the foreseeable future.

Savings vs. Investment Gains

Something I was curious about was my monthly savings rate over this time period versus the amount of this gain that has been directly attributable to the soaring stock market valuations. I also paid off a 0% interest rate promo credit card in April as it was expiring. This credit card payoff is why the liabilities category dropped, while the assets did not increase much for the month.

Over the past ten months, I have contributed:

- $6,000 to my IRAs in a combination of Roth and Traditional contributions.

- $21,794 in employer-sponsored retirement account contributions and 5% match.

- $3,442 in additional savings from coming in under my monthly budget.

That’s a total of $31,236 in contributions to savings, versus a total net worth increase of $48,621. The monthly average of that savings rate comes to about $3,123/month and is right around 60% of take-home pay. I earn the median income for Washington, DC (and live in my own apartment) and readily share with friends and colleagues the ways to drastically reduce your living costs in a high cost of living area. It is not impossible to live on much less than expected if you’re willing to make some smart decisions and find the right deals on housing and transportation.

As you can see, the vast majority of the increase in total net worth was from savings and not investment returns. It’s actually a bit disappointing to see how low my investment returns were over a time period that includes significant stock price appreciation. Part of that is my conservative investment allocation and larger emergency fund. As I’ve been undertaking a relocation recently and another one likely on the horizon, having the extra liquidity in my emergency savings is a comfort thing.

I’ve been aiming for a $3,000/month rate of savings in order to achieve my FIRE goal in about eight years, when my student loans are forgiven via the Public Service Loan Forgiveness program. Smart and steady is the way to FIRE and the core values of The Money Sloth! Cheers!