I’m really not sure where the month of February went. I actually forgot to take a screenshot of my Personal Capital account on the 1st, so I had to use a different method to capture my net worth snapshot than I usually do. Since I am not doing a very good job at producing any content between these monthly update posts, I’ll add a little more commentary than usual here.

In last month’s post I wrote about struggling with the demands of a full-time job and full-time graduate school, while also trying to find time for my internet ventures and some leisure. It turns out there just aren’t enough hours in the day to get to everything anymore. That being said, I am maintaining this level of activity in order to prepare for what’s to come with regards to being forced to return to the office for my job.

At many companies, there is a battle brewing between management and staff with regards to where our work needs to be done. For those like me, I’ve been able to effectively do my job from home for the past two years. I’d even argue my performance is better now than it was in the office, plus I can forgo the commute and other expenses of in-office work. Even with those facts in play, senior leadership at my office is refusing to consider a remote workforce and will eventually force us all back in-person. Because of this inevitability, I want to prepare myself for that situation by increasing my skills (via a Masters degree in a STEM field) and work on growing my internet venture activity to provide for some alternative income. There are three possible outcomes when the showdown with leadership occurs:

- Go back to working in the office.

- Find a new remote job at another company.

- “Retire” early to a much lower cost area and supplement with internet-based income.

I am most likely not willing to consider option #1 any longer. If my job performance would improve from in-office work, or there was some other legitimate reason for my work to be done in-office, then I would consider this possibility. But, it’s now become a principled stance for me and I don’t tend to budge on those. The facts are clear, and unless leadership admits that the only reason they want us to return to the office is for them to feed their need of physical control, then I don’t even have enough respect for them to want to stay in their employ. I have a feeling I am not alone in that sentiment anymore.

Option #3 is becoming very appealing and I have been utilizing the Retirement Planner feature on Personal Capital and the cFIRESim website to model out some different early retirement scenarios.

Net Worth = Assets minus Liabilities

| Assets | Amount | Change from Last Month |

| Checking/Savings | $44,294 | |

| Retirement Accounts | 179,734 | |

| Taxable Investments | 25,788 | |

| Misc. (Gold/Silver/Cash/Collectibles) | 10,200 | |

| Total Assets | 260,016 | +11,043 |

| Liabilities | Amount | Change from Last Month |

| Credit Cards | $5,364 | |

| Student Loans | 196,279 | |

| Total Liabilities | 201,643 | -105 |

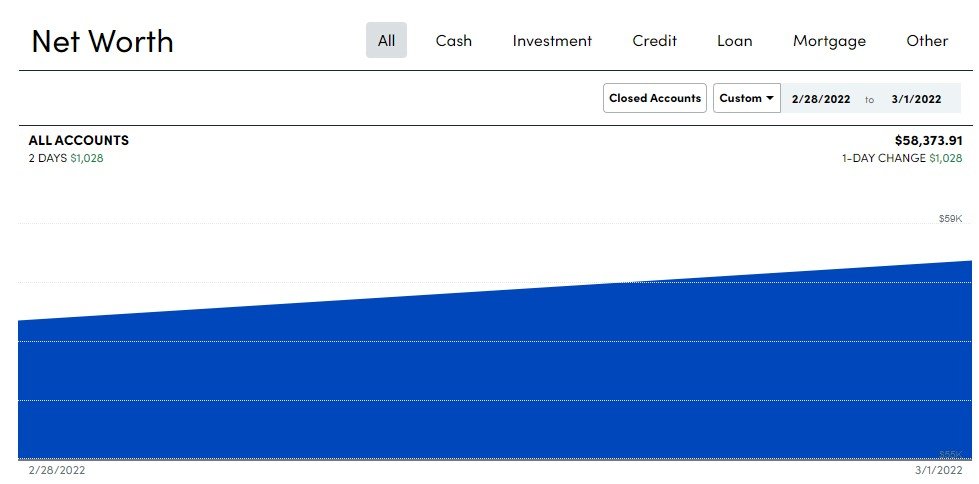

Net Worth = $58,373

Change in Net Worth from last month: +$11,149

Total Change in Net Worth Since July 2020: +$106,601

Net Worth Summary

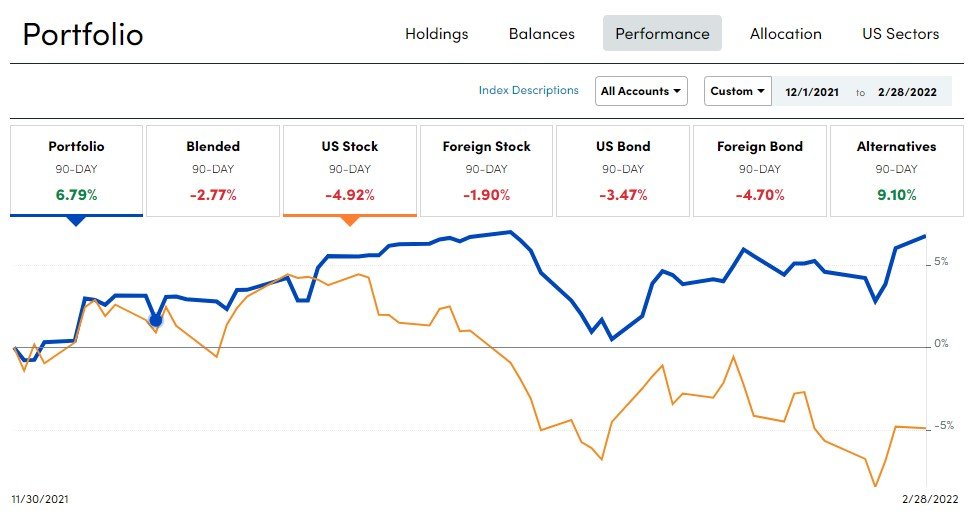

February was a very good month for my investment account balances, despite the S&P 500 falling almost 4% during the month. This is due mostly to a couple of significant investments I made in oil and steel companies prior to the global economic turmoil caused by the Russian invasion of Ukraine. These shares have soared in value as the price of oil and rolled steel has powered higher.

Personal Capital has a pretty cool feature that allows you to track your investment performance compared to numerous benchmarks.

This graph shows the divergence between my portfolio and the S&P 500 as a result of those oil and steel investments, as well as shifting my cash holdings to Activision stock (which is currently trading at a significant discount to the cash buyout price offered by Microsoft and that I fully expect to successfully close). As the broader market declined, the shares of Activision stayed put and the oil and steel investments soared.

My Investments

My own investment strategy has evolved to one where I have the majority of my portfolio invested in index funds and the rest of it is utilized for taking advantage of these unique situations that occur from time to time and provide the possibility of returns greater than the overall market.

In the case of Activision, I had holdings of it prior to the announced buyout offer from Microsoft. However, despite Microsoft offering $95/share in cash, the shares continue to trade around $80 each. This means there is $15/share, or about 19% of upside available in these shares when the transaction closes (expected by June 2023). I added considerably more shares as it sat at $80. Yes, there is risk that the transaction doesn’t close, but I find this to be a much smaller risk than the market is pricing in. Additionally, Activision would receive an enormous payout from Microsoft should the deal not close and that will go straight to the bottom-line for Activision.

For the oil and steel company investments, the unfortunate reality is that it does not appear that the Russian war against Ukraine will end anytime soon, with Russia refusing to admit defeat and atone for their war crimes. Some oil analysts are predicting that crude oil prices could hit $200/barrel if the world shuns Russian crude deliveries. With regards to steel, Russia is (was) the world’s 3rd largest exporter of steel and the continued economic sanctions on their country means a substantial shortage of global steel supplies could occur and the prices of U.S. rolled steel have already begun soaring as a result of these sanctions. With the current US administration’s desire to spend aggressively on infrastructure improvements using American steel, this is even more bullish for the sector.

Because of the uncertainty surrounding my future work/early-retirement plans, I still keep a large emergency fund in cash. Obviously hindsight is 20/20 with regards to how much growth I could have earned in that cash had I invested it, but I am thinking that I should have a large enough cash stash to provide for several years of living expenses in a very low-cost area to give me time to execute a Roth ladder with my retirement accounts. A Roth ladder requires 5 years to start using the funds, so keeping a larger cash cushion can come in handy if early retirement is the option I choose within the next year. One thing I have been doing with this retirement planning in mind is maxing my Roth IRA contributions each year since any funds I deposit there I can remove without penalty (provided I withdraw only contributions and not investment earnings).