Welcome to the two-year anniversary Net Worth Update post from The Money Sloth! It’s hard to believe it has already been two years posting here and while there were some gaps in posting for a period of time, I think things will be back on a regular schedule now. When I started this journey, I had a negative net worth of $-48,228. Today, my net worth stands at $72,511. In two years, I’ve dug myself out of a negative net worth and started on a path to financial independence.

The net worth value does mask the situation a bit as I have a substantial amount of student loans that drag that number down. I have made it about half way through the requirements of the Public Service Loan Forgiveness Program (PSLF). Whether I finish the remaining five years in the future, or whether the program continues to exist at all remains to be seen. Removing those federal student loans from the picture (and assuming debt cancellation at the end of a 25 year income based repayment) the net worth is north of $250,000.

The Purpose of Net Worth Update Posts

I’ve seen some interesting commentary on Finance Twitter about monthly Net Worth Update posts. The debate reminds me of the Rent vs. Buy discussions about primary residences. There are a bunch of very vocal people on each side and seemingly nobody in the middle. I find the net worth update posts to be a way to hold myself accountable and be more proactive with my finances. I continue to post them whether my net worth went up or down (and this month is down).

My last post announced that I quit my job and that means these net worth updates serve another purpose now. Since I no longer have an income contributing to growing my net worth, I am completely dependent on market returns for growth or maintenance of the balance. Keeping a closer eye on my net worth and monthly spending will go a long way in ensuring that I am staying within the range that I need to in order to make it last. Should the market downturn continue through the rest of 2022 and/or 2023, I will have chosen the absolute worst time to leave the labor force as sequence of returns risk will cause significant damage to the longevity of my portfolio. Only time will tell, but my professional opinion is that if a recession occurs it will be caused by media hysteria.

Let’s take a look at where things stand after the final month of my employment:

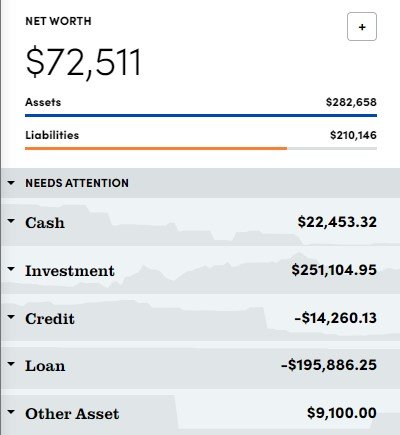

Net Worth = Assets minus Liabilities

| Assets | Amount | Change from Last Month |

| Checking/Savings | $22,453 | |

| Retirement Accounts | 192,581 | |

| Taxable/Nontax Investments | 69,958 | |

| Misc. (Gold/Silver/Cash/Collectibles) | 9,100 | |

| Total Assets | 282,657 | -10,110 |

| Liabilities | Amount | Change from Last Month |

| Credit Cards | $14,260 | |

| Student Loans | 195,886 | |

| Total Liabilities | 210,146 | -496 |

Net Worth = $72,511

Change in Net Worth from last month: -$9,615

Total Change in Net Worth Since July 2020: +$120,739

Net Worth Summary

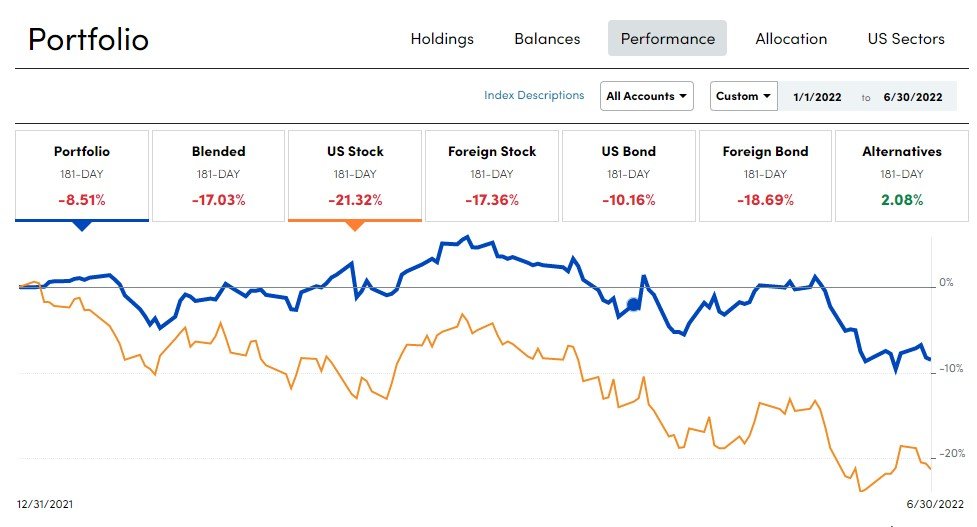

These net worth updates have been a rollercoaster ride lately as the stock market continues it’s turbulent behavior in 2022. Last month saw a nice recovery in the portfolio as a result of some oil stock investments, while June saw those gains erased (and July has been absolutely brutal for oil). What I keep telling myself is that I am down, but not nearly as severe as the overall market and that makes it a little easier to stay the course. I’m also continuing to max out my retirement contributions through the final pay period of my job.

Quitting my job will certainly have an impact on my net worth going forward as I was saving around $5,000 per month into my retirement and investment accounts. That regular investment will be zero starting in August after I get my last paychecks in July.

It’s hard to believe that the overall market is down over 20% through the first half of 2022. That is the worst first half performance of the S&P 500 in over 50 years. The big question now is what happens in the second half of the year. Typically, the market rallies out of these horrific first half performances, but things are a bit dicey this year. Between the Federal Reserve raising interest rates, higher than normal inflation, and paranoia over a recession, it’s anyone’s guess where we end up by the end of December. For now, I’m sitting on a bit of cash and will add to my holdings on the way down as the Fed continues tightening.

Future Plans

I’m taking the first month of my sabbatical to decompress and try to recover from the burnout I experienced in my job as an Economist over the past year or two. I look forward to spending time reading, travelling locally, researching and writing content, starting a new blog (or two), and generally investing in myself for a while. I am also considering pursuing graduate school for a degree in Finance.

As I’ve mentioned before, the ability to take time away from a career to go back to school, start a business, or invest in yourself in some other way is a significant benefit of saving aggressively while you are able to. This financial cushion is the only reason I’m able to explore these other possibilities versus being chained to a 9-5 that may not bring me personal and professional happiness. While I am short of my target for the Retire Early part of FIRE, I have an opportunity to plot a new path for the next 25 years before I hit a traditional retirement age.

I just saw a tweet this morning by @AllOptions_AOC that summed things up perfectly:

“Financial independence is the end of working for the interest of others, and the beginning of a new chapter you can design for yourself.”

Love the the FI topic!

Financial independence ⁰is the end of working for the interest of others, and the beginning of a new chapter you can design ⁰for yourself.

— All Options Considered (@AllOptions_AOC) July 7, 2022