August was a rough month. As I enter my sixth month of working from home and limiting my time outside around people as a result of the Covid-19 pandemic, I noticed my spending ticked higher as a result of some built-up stressors. As someone in a higher-risk category for developing complications from Covid-19, I am extremely thankful for the essential workers who make grocery and food delivery possible. As you’ll see in the breakdown of my spending in August, food was a big increase, as were some other items that will hopefully bring some life and health improvements as I prepare for essentially staying home for the remainder of the year. My employer has refused to give any indication of when we will be returning to the office, but I expect it won’t be until 2021. Many tech companies have already stated they won’t be returning before at least June 2021.

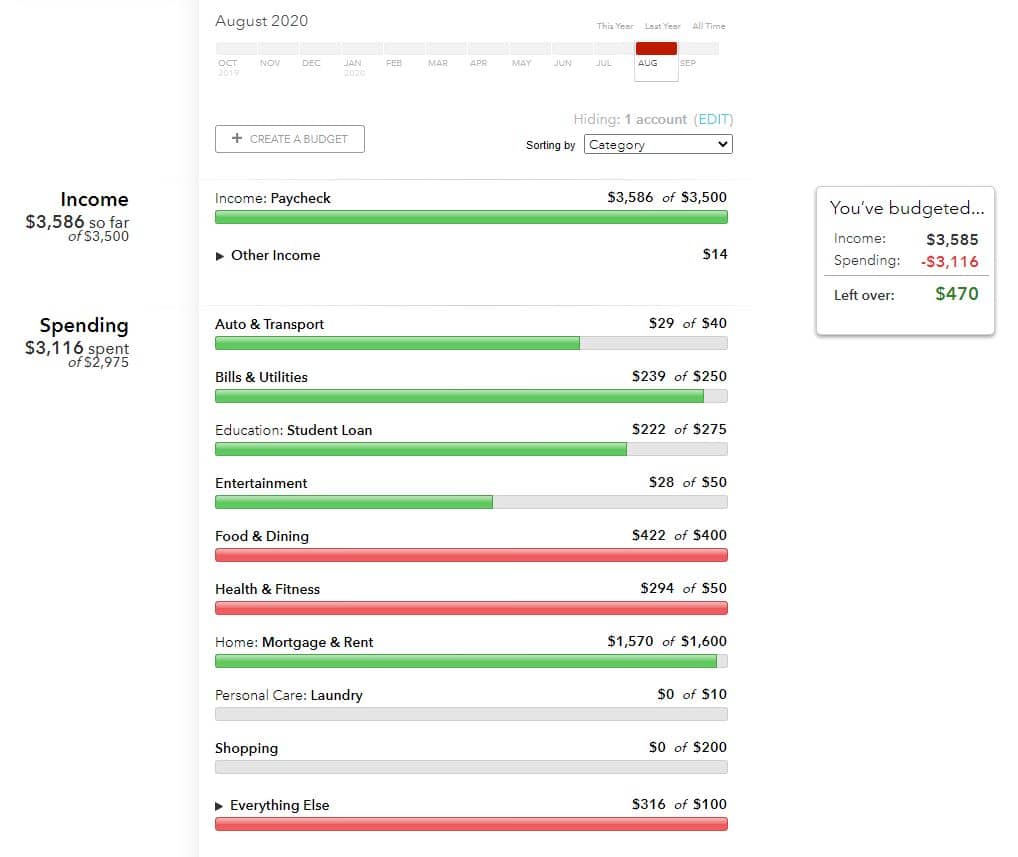

Here are the results of my August 2020 budget:

Budget – Rent

Rent is my largest monthly expense and one of the most consistent. The only variable here is the cost of water which is calculated each month, while the included trash charge is a fixed amount. For August, the total came to $1,570.

Budget – Food & Dining

This is a budget item that has started increasing recently and I ended slightly over my $400 budget this month. I’ve been ordering food from local restaurants much more frequently. Part of this is because so many restaurants are on the brink of failing due to the pandemic and I’m in the fortunate position of having a secure job and want to support my service industry neighbors as best I can. I grew up working in the restaurant industry, starting as a dishwasher in my high school lunchroom and eventually rising to the General Manager level with a national franchise, and know how difficult those jobs can be, not to mention the meager pay that is commonplace in the industry. While this is a part of my budget that is most easily curtailed in order to increase my savings rate, it just doesn’t feel right to cut back here in the current environment.

Budget – Bills & Utilities

Bills and utilities include Internet, TV, cell phone, and electricity. This is certainly an area that I can start exploring some deals to bring the cost down. Unfortunately, the largest of these bills is Internet service and there are very few choices when it comes to service providers authorized to operate in my area. Because I am working from home, it’s also essential that I have a high-speed, reliable internet connection at all times and in this industry you tend to get what you pay for.

Budget – Health and Fitness

Due to the pandemic, I cancelled a fitness class membership that I had previously been using and I’m also not comfortable using the gym in my apartment building as many users fail to follow the gym rules and wearing masks. Because of the lack of physical activity, I have certainly gained the “Covid 20” and have purchased an exercise bike to use in the comfort and safety of my apartment. This should be money well spent, but caused my Health and Fitness spending to go over my budget this month, but this should end up being cheaper in the long run versus paying for a fitness class membership.

Budget – What’s Next?

Despite exceeding my budget in a few categories this month, I’m still happy to say that I manage to live in Washington, DC on about $3,000 per month. By keeping my spending as close to this $3,000 mark as possible, I am on track to save around $30,000 per year in my employer sponsored retirement account, IRAs and taxable investment accounts. I use Mint.com for tracking my monthly spending and unfortunately it does not show the savings rate for retirement contributions that come out of my paycheck, which is why I use Personal Capital to track my net worth over time. This is going to cause some strange numbers to appear in September as I have increased my employer retirement contributions in order to hit the 2020 maximum of $19,500.

SlowFI

Something the Covid-19 pandemic, and the current political environment, has taught me is that one of the most important things a person can do for themselves is to be financially independent. Financial independence brings choice and the ability to make significant changes in your life in response to your environment. However, as part of this journey, I’m also seeing the value in a “SlowFI” approach to reaching financial independence. Especially when the world around you is stressing you out, it’s important to take care of your mental and physical well-being in the present, even if it means pushing that FI date out a little bit… you must enjoy the FI journey otherwise, I have to ask, what the hell is the point?