This net worth update is quite late, but I’m still getting it done before the end of the month! A lot has happened in the past month, including my employer demanding our return to the office. During the Covid-19 pandemic, I moved 1000 miles away from my office location and expected that we would be able to continue working from home as an option indefinitely since it was incredibly effective for myself and many coworkers. We routinely received high praise from management regarding all of our achievements during the two years we worked exclusively from home. Unfortunately, the leadership at my employer now REALLY wants to force everyone back to the office. I honestly don’t know why they want to do this, other than because they feel like they don’t have anything to do and think managing/leading is walking up and down the hallways.

After formally requesting that I be re-classified as a permanent remote worker, there still wasn’t a decision made after a month so I submitted my resignation notice. I’m just not interested in moving back to a very high cost of living area with such a modest salary.

Because of this new development, I’ve made some tweaks to my net worth calculation to make it better reflect my assets that will be available to me when I leave the workforce. For example, I currently pay into a pension plan that I would not want to keep if I were to leave this job so many years before my eligibility for collecting it. These mandatory contributions are able to be rolled over into a Roth IRA that I control and would be a great addition to my early retirement planning.

I’m also working on modeling out some cost of living scenarios for a few international locations where my retirement savings could stretch much further than in the United States. Be on the lookout for these posts in the future. This sloth may be planning a relocation to a more suitable climate!

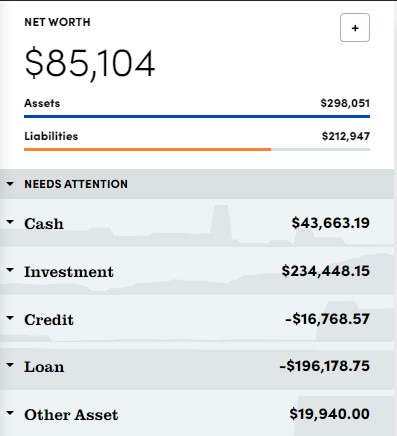

Net Worth = Assets minus Liabilities

| Assets | Amount | Change from Last Month |

| Checking/Savings | $43,663 | |

| Retirement Accounts | 189,225 | |

| Taxable/Nontax Investments | 55,513 | |

| Misc. (Gold/Silver/Cash/Collectibles) | 9,650 | |

| Total Assets | 298,051 | +38,036 |

| Liabilities | Amount | Change from Last Month |

| Credit Cards | $16,769 | |

| Student Loans | 196,178 | |

| Total Liabilities | 212,947 | +11,305 |

Net Worth = $85,104

Change in Net Worth from last month: +$26,731

Total Change in Net Worth Since July 2020: +$133,332

Net Worth Summary

March was another good month for my investments as the holdings in oil and steel companies have significantly outperformed the broader market. I also made a tweak to include the cash balance of my pension contributions in my net worth calculations since I would roll these over into a Roth IRA when I leave my current employment. This had a positive effect of about $10,000 that grows at about $350/month. Had I not started including this, the net worth increase this month would have been closer to $17,000 instead.

The increase in liabilities is the result of taking advantage of a 3% for 21 month credit card offer. In this inflationary environment, I couldn’t resist borrowing at a sub-2% APR and investing it in something reasonably safe that will earn a higher return.

It appears that I am quickly approaching the second anniversary of The Money Sloth and am on track to reach a total increase in net worth of around $150,000 in 24 months. I never would have imagined it was possible before embarking on this journey. It turns out that a (mostly) frugal lifestyle and consistent saving and investing can pay significant dividends.

I did some quick math on my current monthly budget and I’ve been able to increase my savings rate to a little over 60% of my gross monthly income in 2022. I’ve also cut back to only working one job this year as well. Working remotely has cut so many expenses out of my monthly budget, it’s astonishing. For office workers whose job is not customer-facing, this could be the quickest way to building up investment balances quickly.